All Categories

Featured

Table of Contents

A PUAR enables you to "overfund" your insurance plan right approximately line of it ending up being a Modified Endowment Contract (MEC). When you make use of a PUAR, you quickly enhance your money value (and your survivor benefit), thereby raising the power of your "bank". Even more, the more cash worth you have, the better your passion and dividend settlements from your insurer will certainly be.

With the surge of TikTok as an information-sharing platform, monetary guidance and strategies have actually found an unique means of spreading. One such technique that has been making the rounds is the unlimited banking idea, or IBC for brief, gathering endorsements from celebs like rapper Waka Flocka Flame. While the technique is currently popular, its origins map back to the 1980s when financial expert Nelson Nash presented it to the globe.

What are the risks of using Wealth Building With Infinite Banking?

Within these policies, the cash worth grows based on a rate established by the insurance provider (Infinite Banking retirement strategy). When a significant cash money value gathers, insurance holders can obtain a cash money value finance. These fundings differ from traditional ones, with life insurance policy acting as security, indicating one can shed their insurance coverage if borrowing exceedingly without ample cash money value to sustain the insurance coverage prices

And while the appeal of these policies is apparent, there are innate restrictions and dangers, necessitating thorough cash money worth tracking. The method's legitimacy isn't black and white. For high-net-worth individuals or local business owner, particularly those making use of techniques like company-owned life insurance (COLI), the benefits of tax obligation breaks and compound development could be appealing.

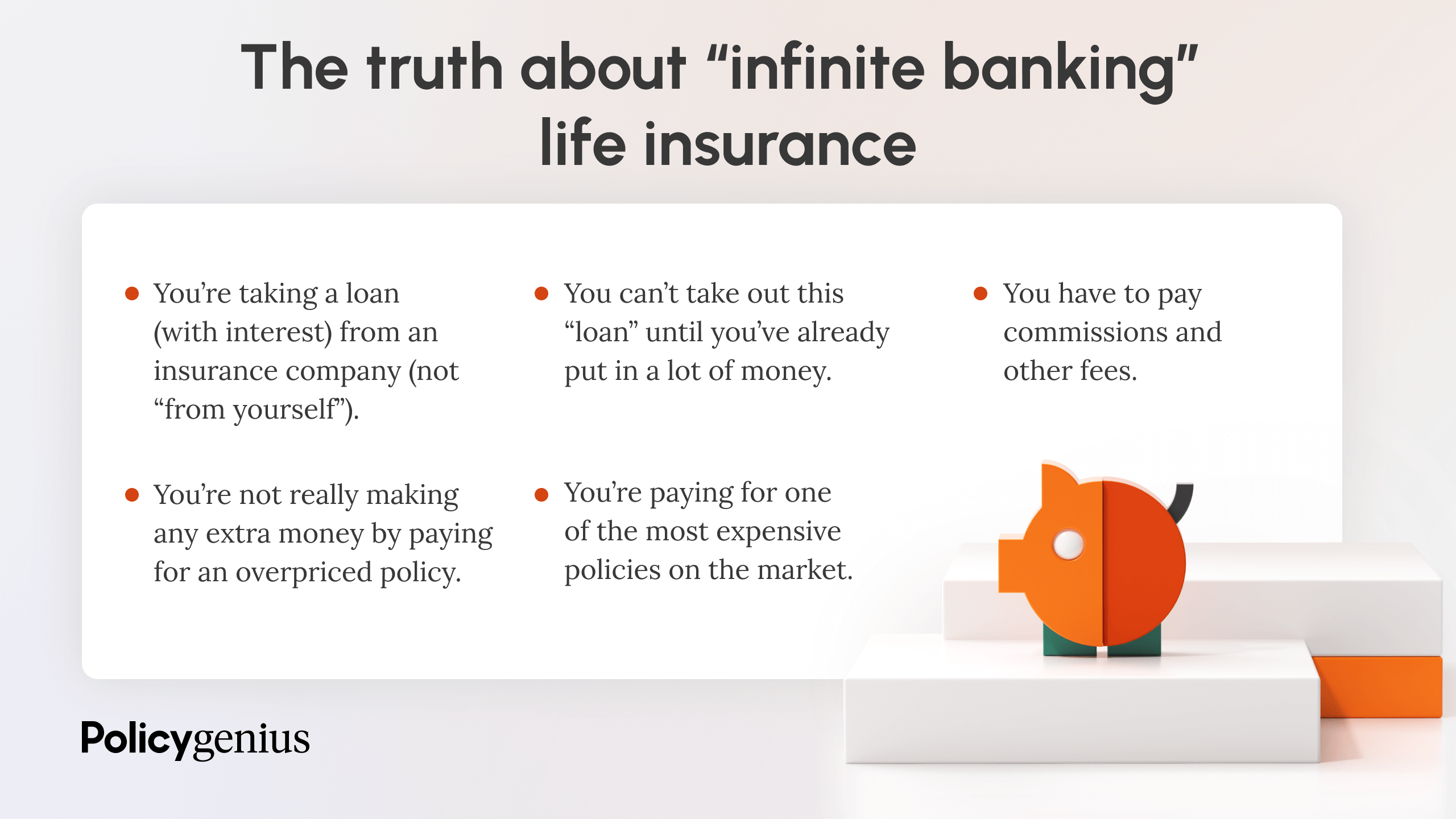

The attraction of unlimited financial does not negate its difficulties: Price: The foundational requirement, a permanent life insurance policy plan, is pricier than its term counterparts. Eligibility: Not everyone receives entire life insurance policy as a result of extensive underwriting procedures that can omit those with specific health or way of life problems. Complexity and risk: The elaborate nature of IBC, combined with its risks, might prevent many, specifically when easier and much less risky choices are readily available.

What makes Infinite Banking For Financial Freedom different from other wealth strategies?

Alloting around 10% of your month-to-month earnings to the plan is just not possible for most people. Part of what you read below is merely a reiteration of what has actually currently been stated over.

So before you obtain into a scenario you're not planned for, know the complying with first: Although the principle is typically sold therefore, you're not actually taking a lending from yourself. If that were the instance, you would not have to repay it. Rather, you're obtaining from the insurance provider and need to repay it with passion.

Some social media sites posts advise using money worth from entire life insurance policy to pay for credit score card debt. The idea is that when you pay back the loan with passion, the amount will be returned to your financial investments. That's not just how it works. When you repay the funding, a portion of that interest goes to the insurance policy company.

For the initial numerous years, you'll be repaying the payment. This makes it exceptionally hard for your plan to collect value throughout this time around. Entire life insurance prices 5 to 15 times much more than term insurance. Most individuals simply can't afford it. So, unless you can pay for to pay a few to numerous hundred dollars for the following years or even more, IBC won't work for you.

Is Infinite Banking a better option than saving accounts?

If you need life insurance policy, below are some useful tips to consider: Think about term life insurance coverage. Make certain to go shopping around for the finest rate.

Envision never having to stress about bank finances or high interest prices once again. That's the power of limitless banking life insurance policy.

There's no set funding term, and you have the liberty to decide on the repayment schedule, which can be as leisurely as paying off the funding at the time of death. Infinite Banking vs traditional banking. This flexibility includes the servicing of the lendings, where you can select interest-only settlements, maintaining the lending equilibrium level and manageable

Holding cash in an IUL taken care of account being attributed interest can usually be better than holding the cash money on deposit at a bank.: You have actually always desired for opening your own bakeshop. You can borrow from your IUL policy to cover the initial expenditures of renting an area, purchasing tools, and employing staff.

What are the tax advantages of Infinite Banking Concept?

Individual car loans can be gotten from conventional banks and credit history unions. Borrowing cash on a credit score card is typically really costly with yearly percentage prices of rate of interest (APR) commonly getting to 20% to 30% or even more a year.

{kind=link}

Latest Posts

Becoming Your Own Banker Nash

Infinite Banking - Be Your Own Bank - Insure U4 Life

Cash Flow Banking Reviews